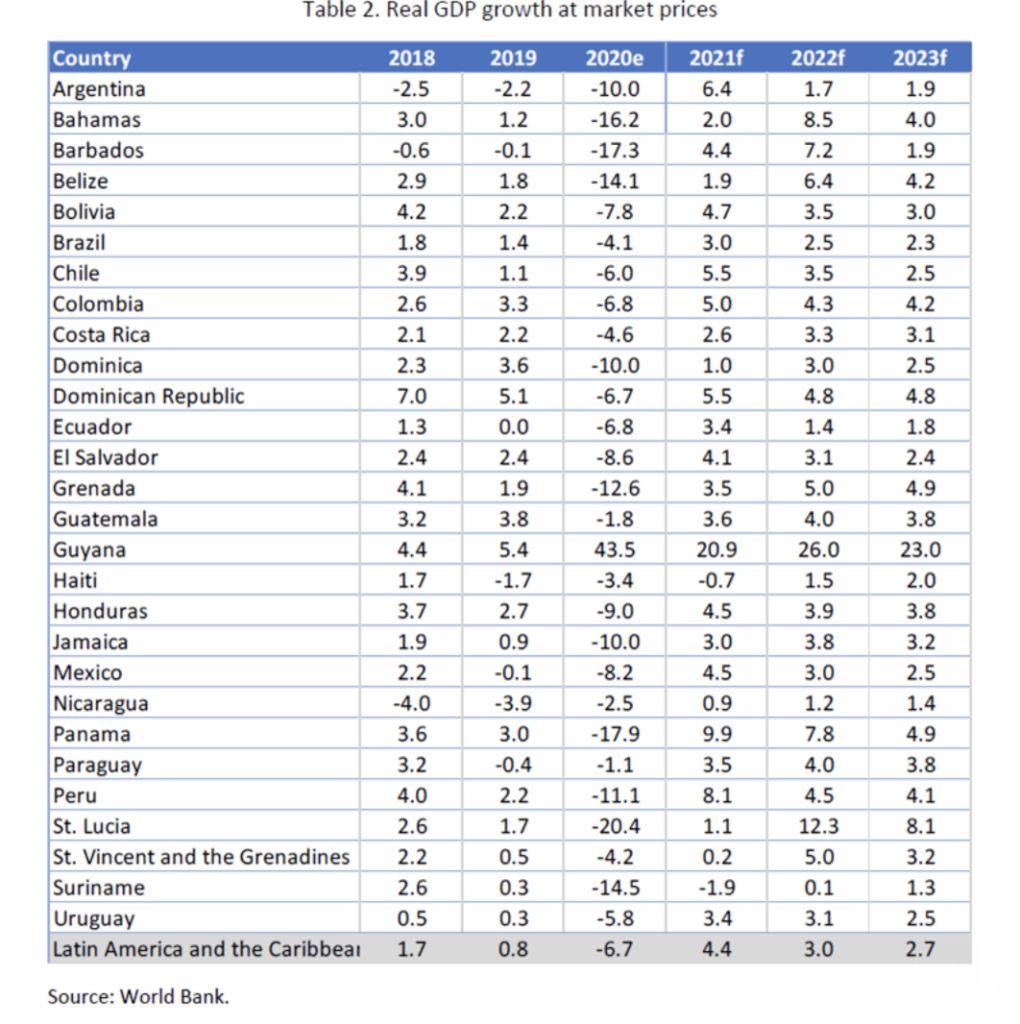

Latin America and the Caribbean (LAC) suffered more damage to health and the economy from the COVID-19 pandemic than any other region, but as the region begins to rebound, the opportunity for transformation opens significant in key sectors, according to a new World Bank report that estimates a 9.9% growth for Panama in 2021, only surpassed by Guyana.

Due to the pandemic, the Gross Domestic Product (GDP) in the Latin American and Caribbean region (except Venezuela) fell 6.7% in 2020. A return to growth of 4.4% is expected for 2021. In comparison with the Bank’s projections at the end of 2020 of a fall of 7.9% by 2020 and a GDP expansion of 4.0% by 2021.

The COVID-19 crisis will have a long-term impact on the economies of the region. Lower levels of learning and employment are likely to reduce future earnings, while high levels of public and private borrowing can strain the financial sector and slow down the recovery.

Despite these challenges, there are positive areas. International trade in goods remained relatively good, despite the sharp decline in trade in services, particularly tourism.

Most commodity prices are higher than before the COVID-19 crisis, partly thanks to China’s early recovery. This is a good thing for exporters of agricultural and mining products.

Likewise, capital markets remained open for most of the countries in the region. In fact, debt taking abroad increased, helping to mitigate the economic and social impact of the COVID-19 crisis. Most countries in the region have run significant budget deficits since the beginning of the pandemic.

For example, hotel and personal services can suffer long-term damage, although information technology, finance and logistics will expand. In the medium term, the gains may be greater than the losses.

Technology is also an opportunity to transform the energy sector. Latin America and the Caribbean has the cleanest electricity generation matrix of all developing regions, mainly due to the abundance of hydroelectric energy. And thus, it should have the cheapest electricity in the developing world, but instead has the most expensive, essentially due to inefficiencies.

Businesses and households in the region pay much more for the electricity they consume than it would cost to generate it. These inefficiencies are reflected in frequent blackouts, technical and commercial losses, overstaffed public companies, and abuses of market power by private generators.

With an appropriate institutional framework, technology can increase competition in the sector, thereby reducing the price of electricity and increasing the share of renewable energy. Distributed generation can make companies and households depend on their own energy sources, such as solar panels, and buy or sell electricity on the grid depending on the time of day.

Additionally, an increase in cross-border electricity trade can take advantage of differences in installed capacity, generation costs, and demand seasonality to generate mutual benefits.

However, this efficiency improvement will only take place if electricity can be bought and sold at an appropriate price.

While there are signs that the region’s economies are recovering and hopes that this upheaval will have some positive outcome, the outlook for this year remains uncertain.

Leave a Reply